Content

- How to Use This Accounting Terms Guide

- Equity Method

- Pros and Cons of the Cost Method of Investments

- Equity Method of Accounting Example, Part 1: Purchasing a Minority Stake and Recording Net Income and Dividends from It

- Home / Resources / Streamlining Equity Method Accounting and Equity Pick Up

- Equity Method vs Consolidation Method (Accounting) – Explained

Instead, the investor is entitled to a percentage of the company’s profits. When calculating equity in accounting, the company’s assets are offset by its liabilities. Equity in accounting comes from subtracting liabilities from a company’s assets.

- She earned a bachelor of science in finance and accounting from New York University.

- The equity method is an accounting technique used by a company to record the profits earned through its investment in another company.

- However, publicly traded companies whose securities fall under SEC regulations must use GAAP standards.

- These assets include real estate with a carrying amount of $20m and a fair value of $35m, with a remaining useful life of 15 years.

- The terms and concepts in this guide were curated in part for their relevance to new entrepreneurs.

- Under the cost method, you make no accounting entries regarding investee OCI.

Accounting is the process of tracking and recording financial activity. People and businesses use the principles of accounting to assess their financial health and performance. Accounting also serves as a useful way for people and companies to honor their tax obligations. Assets include almost everything owned and controlled by a company that’s of monetary value and will provide future benefit. Assets are classified by how quickly they can be converted to cash, whether they are tangible or intangible, and how a business uses them.

How to Use This Accounting Terms Guide

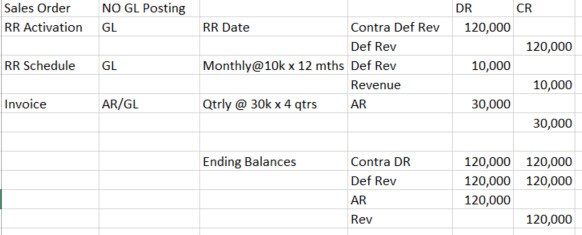

Generally, ownership of 50% or more of an entity indicates control, but entities must use significant judgment and additional criteria before making the final ownership determination. The equity method is a type of accounting used for intercorporate investments. It is used when the investor holds significant influence over the investee but does not exercise full control over it, as in the relationship between a parent company and its subsidiary. The $12,500 Investment Revenue figure will appear on ABC’s income statement, and the new $210,000 balance in the investment account will appear on ABC’s balance sheet. The net ($197,500) cash paid out during the year ($200,000 purchase – $2,500 dividend received) will appear in the cash flow from / (used in) investing activities section of the cash flow statement.

A business chooses its accounting method depending on which is right and works best for the company and its owner. Receive timely updates on accounting and financial reporting topics from KPMG. Equity financing can give aspiring business owners the capital needed to realize their dreams. This means they might have to give the other investors a say in decisions about how to run the business. Investors recognize the dividends they receive from investees as a reduction in the carrying amount of their investments rather than as dividend income. Since 2018, FASB has appeared to be moving toward a change that would allow companies that buy another business to amortize or write down goodwill impairments to zero over time.

Equity Method

Fixed assets are those that have a longer lifespan – generally over one year. Keeping track of assets can be challenging given the number and diversity of assets a company https://kelleysbookkeeping.com/ may own. Automated asset management solutions offer a way to inventory, categorize and track assets in order to understand their value and plan operations efficiently.

The cost method is an accounting method in which investment securities are carried at historical cost. Historical cost is the original price of an asset, plus any subsequent costs incurred to keep the asset in working order. The cost method is applied in many financial accounting instruments, including investments and fixed or inventory assets. It is a conservative accounting method when the investor owns no more than 20% of the company’s investment.

Pros and Cons of the Cost Method of Investments

A common example of such an arrangement is several companies forming a joint venture to research and develop a specific product or treatment. Under a joint venture, the entities can pool their knowledge and expertise, while also sharing the risks and rewards of the venture. Each of the participating members have an equal or near equal share of the entity, so no one company has control over the entity at the formation of the joint venture. However each is able to significantly influence the financial and operational policies of the entity. In this scenario, the partners will account for their investment in the joint venture as an equity method investment. When the investee company pays a cash dividend, the value of its net assets decreases.

Although the following is only a general guideline, an investor is deemed to have significant influence over an investee if it owns between 20% to 50% of the investee’s shares or voting rights. If, however, the investor has less than 20% of the investee’s shares but still has a significant influence in its operations, then the investor must still use the equity method and not the cost method. Introduction to accounting frequently identifies assets, liabilities, and capital as the field’s three fundamental concepts. Assets describe an individual or company’s holdings of financial value. In accounting, liquidity describes the relative ease with which an asset can be sold for cash. Assets that can easily be converted into cash are known as liquid assets.

Equity Method of Accounting Example, Part 1: Purchasing a Minority Stake and Recording Net Income and Dividends from It

But not all small business owners can pursue formal financial training. Some students enter accounting programs with little technical knowledge — and that is OK. This guide is an easy-to-use resource for developing the vocabulary accounting professionals use.

- A common example of such an arrangement is several companies forming a joint venture to research and develop a specific product or treatment.

- But it records nothing else from Sub Co., so the financial statements are not consolidated.

- Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future.

- Once the investor determines the type of investment and the applicable accounting treatment, it is time to record the equity investment.

- You treat dividends as a return of investment by posting to a contra-asset account linked to XYZ Corp. securities, thereby reducing the net carrying value of the investment.

- If an investor exercises neither control nor significant influence over the acquiree, the proper method of accounting for the investor is the fair value method.

Accountants also distinguish between current and long-term liabilities. Current liabilities are liabilities due within one year of a financial statement’s date. Equity Method Definition & Example Long-term liabilities have due dates of more than one year.The term also appears in a type of business structure known as a limited liability company (LLC).

Typically, assets are valued by the expected future cash flows they represent in their current condition, according to the IFRS. They are categorized based on specific characteristics, such as how easily they can be converted into cash (for company-owned assets) and their business purpose. They help accountants assess a company’s solvency and risk, and they assist lenders in determining whether to loan money to a company. The cost method is the simplest and most common method used to account for investments.

Such an investor has very little or no influence on the investment, which is recorded in a balance sheet in the asset section. On 1 January 20X1, Entity A acquired a 25% interest in Entity B for a total consideration of $50m and applies the equity method in accounting for it. Entity B’s net assets as per its financial statements totalled $150m.

When do you apply the equity method?

Accounting for equity method investments can be quite complicated, but this article summarizes the basic accounting treatment to give you a high level understanding. The investor’s proportionate share of the investee’s AOCI is written off against the remaining carrying value, also contributing to the calculation of the carrying amount of the “new” asset. If the investor’s amount of adjustment to AOCI exceeds the equity investment value, the excess will be recorded to the income statement as a current period gain. On the other hand, the fair value method requires frequent adjustments to reflect the changing value of the underlying investment with the current market changes. The cost method differs from the equity method in that it does not require the investor to adjust the investment for their share of the underlying company’s earnings or losses. This means that any gains or losses on the investment are only recognized when it is sold.